|

|

The Goldenbar Report Gold, Yields, and PE's A Goldenbar Editorial |

| Print Copy |

|

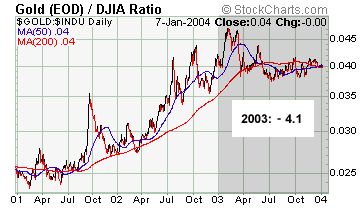

It was their best yearly gain in almost a decade. Gold prices gained 20%. It was the first year in four (since 1999) that the Gold / Dow ratio fell. Before Dow bulls run away with enthusiasm, they should know that it is very rare for this ratio to be down so little in years when the Dow puts in such gains. Usually it plunges. Drops of about 25% were common in the nineties during bullish Dow years. In 1997 the ratio dropped almost 40% for example. What's more, in my own personal data, I use the average monthly price - determined by the mean of the high and low for the month. According to this data, the Gold/Dow ratio is up almost 5% in 2003.

What does it mean? First, annual comparisons aren't relevant merely at yearend. It's just as important for instance to look at how this ratio performed from precisely the April 2003 to the current period - which is more proximal to the period in which the Dow actually rallied. Though even here, during the Dow's best months you can see that gold would hold its own. We're going to show you lots of good pictures today in order to try and shed some light on the meaning of the behavior of this relationship past, present, and future. Specifically, we're going to present a case for much leaner stock market valuations (PE or otherwise - all valuation models follow the same general trends in a time-series). The conclusion is thus apparent. The Dow is overvalued, rather than gold. As you will soon see, there are generally two kinds of profit booms in the United States. Those that occur amid a weak US dollar (commodity type boom), and those that occur amid a strong US dollar (financial or tech boom - disinflation theme). Gold itself tends to lead the former kind. It is because the significance of the gold rally to date has not been played out in the bond market, that our conclusion is that the Dow is overvalued, rather than that it is gold which is overvalued. The Federal Reserve staff are busy patting themselves on the back for their success in 2003 (see our last issue; subscribers). Greenspan claims success in the Fed's handling of the bubble-aftermath, but also gave the economy some credit. Fed governor Bernanke rationalized the Fed's accommodative interest rate posture in the face of the signs of an upturn, the weak dollar, and strong commodity prices by suggesting that it should target the weak labor market. (http://www.federalreserve.gov/boarddocs/speeches/2004/20040104/default.htm) Trouble is, we'd argue that the labor market is weak structurally because profusely easy monetary policies have continued to postpone the correction necessary to rid the economy of its malinvestments (to heal itself), while adding to its underlying misery. Hence, the implications of Bernanke's comments are hugely bullish for gold (if they carry any weight, which we suspect they do) because they refuse to acknowledge not just this, but also any price and interest rate risk in an environment of soaring gold prices. The so-called Hawkish Fed of the nineties is now the Inflationist Reichesbank. C'mon, they can't even define inflation right. But don't get your twinkies in a knot. It's just a metaphor. The odd dip in money supply growth notwithstanding, money supply grows virtually year in and year out. However, we've got an environment today where gold and commodity prices are rising fast, and where the US dollar is falling just as fast. These things are connected to money supply, but not directly. Sometimes the US dollar goes up regardless of this inflation - if commodity prices happen to be falling, and stock and bond market returns are higher than they are in other currency denominations for instance. But this is not the case today. The Fed likes to think that conditions at the moment present no danger to their aim of price stability, but just in case they do, Mr. Bernanke is telling us that they don't mind higher growth rates in prices now ("Inflation is not simply low; for my taste, it is very nearly at the bottom of the acceptable range for (measured) inflation" - Bernanke). Hopefully, by the time you've finished looking at these graphs you'll be able to reckon why the Fed's policies are producing the kind of boom that makes their policy of low interest rates untenable, and why in fact the policy can only accelerate the variables that undermine stock and bond returns. This is besides any contribution of the government's budget predicament. To understand the significance of stronger gold prices, it's often helpful to look at it in the context of history (I could only get monthly gold price data to the beginning of 1980, but the cyclical relationships are sufficient to make our point). When gold is rising as fast as it is, it means at least that money is too easy, and will eventually lead to higher prices and interest rates. Any profits resulting from this monetary influence should be suspect, because they arise from currency debasement (more obviously than usual), which is reflected in interest rates as discovered. Hence, gold leads both the CPI and bond yields, and as you can also see below, it's hardly ever wise to wait until the growth rate of the CPI begins to reflect inflation before buying gold.

Sometimes the data doesn't behave as usual. This is one of those times, or at least it was before June - arguably when bond yields finally bottomed. Depending on where you put gold's bottom, they (yields) are either two years or six months past due. If June was the bottom in yields it occurred precisely two years after the 2001 bottom in gold prices. In any case, it's rare for gold to be so well into a move without as much as a hiccup in yields. It's a divergence, and so long as the Fed remains unbothered, the divergence can only resolve by higher yields (because gold will just keep rising). So if history serves us correct, the CPI and bond yields should start heading up soon, and are in fact overdue to do so. But what does that mean for the stock market? Earnings for the S&P - if they come in as expected at yearend - are going to be up 90%. The comparison is favorable since earnings are coming off a trough that resulted from the steepest drop in profits since the thirties. Still, even with that gain, the five year annual growth rate in S&P 500 earnings is but 6% (compounded rate), while the market's PE ratio remains stubbornly high at over 20. What's more, the nature of that profit gain is dubious. Not just because the currency is debasing - which is true - but also because of what that entails for interest rates, as we've shown, thus PE ratios (equity values) as we are about to show. The inverse relationship between yields and equity values is evident on a long term chart of the S&P 500 PE versus the 10 year bond yield (constant maturity):

Naturally, these are long term cycles. But we're arguing that the current one is about to reverse, because we're arguing for a bull market in gold, and higher interest rates. As you can see in the chart above, the last important (or secular) contraction in PE's occurred from about 1960 to 1980, during the last big bear market in bonds, which came about because of the Fed's monetary policies during the fifties where they similarly and unsuccessfully tried to cap bond yields, and stoke inflation (yes they try). Ultimately that would undermine Bretton Woods, which was doomed anyway since it was a phony standard to begin with. We have to take into account that the US dollar floats today, so the only arrangements subject to breaking are those we don't know about. Clearly, the pressure on the dollar is enormous, and any arrangement is ultimately subject to the market anyway. The relationship between prices and interest rates should be as evident as the relationship between the currency and prices. The relationship between interest rates and PE ratios is that valuations of future earning streams are dependent in part on the rate of interest. If investors demand more yield out of their bond, the returns in stocks are going to have to be more competitive, which requires either that they are, or that earnings yields go up (which means PE's go down). There are two questions that come to mind: 1) why can't stocks just always go up if the weak dollar can stimulate profits, and 2) is there anything special about this recovery that justifies a 26 times earnings multiple (PE)?

According to the data in the chart above, the answer to #2 is obviously no. The nineties' profit boom wasn't any better than the rest (see data in graph). I am categorizing a profit boom according to periods where profits grew fastest. In fact, as you can see, most profit booms in the United States tend to peak out at an annual rate of growth in the neighborhood of 12 to 15 percent (1987-1989 the exception). Therefore, the most satisfactory explanation for the currently high (by historical standards) stock market PE ratio lies in the previous chart - i.e. the last time yields were in this range, PE's were too. Naturally the question is, how long can yields remain in this range... to which you know the likely answer. More importantly, look at the growth in profits during the seventies era in the chart above, compare it to the 1994-2000 period and try and come to a coherent explanation for why PE ratios in one period are high and in the other are low. Dollar devaluation. Indeed, PE ratios aren't only inversely correlated to interest rates, they are directly correlated to the dollar - especially with regards to its commodity value. Bear with me. Although I won't replicate the chart here, we've shown a chart of the CRB and other commodities that go back to the late 19th century along with Robert Shiller's (Irrational Exuberance) estimate of the S&P 500 PE ratio going back to 1876. There were three commodity booms: 1896-1919, 1933-1947, and 1969-1980. These are the US dollar's three secular devaluations during the 20th century. They can be confirmed in other ways, but the dollar was mostly fixed against other currencies until 1971. According to Shiller's data, the S&P's PE ratio contracted three times also: from 1895 to 1918, 1929-1949, 1960-1980 (as above). Let me make it simple. If gold leads interest rates and prices, then if we're right about a gold bull market, interest rates are destined to rise. When interest rates rise - especially if they indicate a new long term trend reflecting the growth of inflation expectations during a secular dollar debasement - stock market "values" should contract. So long as the Fed remains oblivious to the true nature of inflation risk today it'll remain bullish for gold prices, and hence can only strengthen our case against stock and bond prices. Lastly, high PE ratios also impact another way. If they are high, but not rising, they tend to act as a limit to the upside in stock outlooks or returns generally, which can weigh on the currency even more to the extent that its value is determined by relative real returns between currencies, and especially in an environment where the gains in gold make the nature of any gains in stock prices or profits suspect in the first place. The answer to the first question above then (why can't stocks just always go up if the weak dollar can stimulate profits indefinitely) is twofold: a) interest rates head them off, and b) if the profits aren't good quality, investors value them differently - in both cases it means lower PE's (or whatever model of earnings value). Nonetheless, once PE ratios finally contract, assuming the commodity boom continues the commodity related stock sectors (like gold, metals, and oil shares) should begin to dominate the market averages in terms of capitalization. At this point, from the lower PE, the averages can again be put on a path where the growth rate in commodity profits can sustain a new bull cycle, at least until yields rise far and fast enough to make even that boom unsustainable, as was the case in late seventies/early eighties. But Bernanke is no Volcker. The 2004 Fed is opposite to the Volcker Fed. It is pro-inflation. The reason is not to be found in the character of the Fed chairman or any other single person in my view, but rather, in its current policy predicament. By the time Volcker got into office, stock market PE ratios were already beaten down, and bonds were on their 28th year of a bear market. They had nothing to lose by then! Today it's opposite. The Fed can't raise rates. It can't step in front of the market and lead rates higher to head off the inflationary boom. Greenspan said as much in his speech, claiming it's not even the Fed's job to recognize or halt a boom - of any kind. Only, he doesn't say they can't, he says they won't, or shouldn't. We say they can't. If they did, they'd be out of business. Even the admission that there is inflation risk at this point of historic extremes in yields and PE ratios would cause the Dow to crash. The Fed could only hasten its troubles if it implemented any kind of tight monetary policy today. It's a virtual inflation trap! So the fact that the Dow beat gold out in 2003 by a small margin should not provide comfort to any Dow bull. It only supports our contention that the implications of gold's bull market - inflation, inflation, and more inflation, have yet to manifest in stock and bond values.

|

| The GoldenBar Report is not a registered advisory service and does not give investment advice. Our comments are an expression of opinion only and should not be construed in any manner whatsoever as recommendations to buy or sell a stock, option, future, bond, commodity or any other financial instrument at any time. While we believe our statements to be true, they always depend on the reliability of our own credible sources. We recommend that you consult with a qualified investment advisor, one licensed by appropriate regulatory agencies in your legal jurisdiction, before making any investment decisions, and barring that, we encourage you to confirm the facts on your own before making important investment commitments. |

| Copyright©2003 - The GoldenBar Report |

So

maybe it's more like a neck and neck race.

So

maybe it's more like a neck and neck race.